How I Beat Debt While Predicting Market Shifts—A Real Story

Paying off debt felt impossible—until I started connecting the dots between my spending, savings, and what was really happening in the economy. I wasn’t a trader or a financial expert, just someone drowning in balances and tired of quick fixes. Then I discovered how understanding market trends could actually guide smarter debt repayment. This is how I turned financial chaos into control, one realistic step at a time. What began as a desperate effort to stop falling behind became a structured journey of awareness, discipline, and strategic timing. The real shift wasn’t just in my bank account—it was in my mindset.

The Breaking Point: When Debt and Uncertainty Collided

There was a moment, not long ago, when I sat at my kitchen table staring at a stack of credit card statements, loan notices, and overdue bills, feeling utterly defeated. The numbers hadn’t changed in months, despite cutting back on dining out, canceling subscriptions, and selling things I no longer needed. I was making payments—sometimes more than the minimum—yet the debt barely budged. The interest kept growing, the cost of groceries climbed, and my part-time hours at work had been reduced. It wasn’t just the money that was slipping away; it was my sense of control.

That period marked my breaking point. I had followed the standard advice: create a budget, stick to it, and pay extra whenever possible. But life kept interfering. A surprise car repair wiped out a month’s progress. Then, a rent increase made my carefully balanced spreadsheet obsolete. I began to suspect that something larger was at play—something beyond my personal choices. I wasn’t lazy or irresponsible, but I felt like I was failing anyway. The emotional toll was heavy: sleepless nights, constant anxiety, and a growing sense of shame that made me avoid checking my accounts altogether.

What I didn’t fully grasp at the time was that personal finance doesn’t operate in isolation. It’s deeply influenced by broader economic forces—inflation, employment trends, interest rates, and consumer confidence. These aren’t abstract concepts discussed only on financial news channels; they directly affect how much your money is worth, how expensive borrowing becomes, and how secure your income feels. I had been trying to fix my finances with only half the picture. My budgeting efforts were like bailing water from a boat without noticing the hole beneath the floorboards.

The turning point came when I read a short article about rising interest rates. It mentioned that the central bank was considering rate hikes to combat inflation. At first, it seemed irrelevant to me—I wasn’t investing or running a business. But then I looked at my credit card APRs and realized they were variable. A rate hike would mean higher interest charges, making my debt even harder to pay down. That was the first time I saw a direct link between national economic trends and my personal financial struggle. I wasn’t just battling bad habits; I was navigating a shifting financial landscape without a map.

Rethinking Repayment: Why Market Awareness Matters

For years, I believed debt repayment was a purely personal challenge—one that required willpower, discipline, and a strict budget. While those elements are important, I began to understand that timing and context matter just as much. Just as a farmer doesn’t plant seeds in the middle of winter, a borrower shouldn’t make major financial moves without considering the economic season. Market awareness doesn’t mean becoming a Wall Street analyst; it means recognizing that financial decisions don’t happen in a vacuum. External conditions can either support your progress or quietly undermine it.

Take interest rates, for example. When rates are low, it’s often a good time to consolidate high-interest debt or refinance a loan. Locking in a lower rate can save thousands over time and make monthly payments more manageable. But when rates are rising, as they were during my breaking point, aggressive repayment strategies may need to be adjusted. Throwing extra money at a credit card with a variable rate during a rate hike cycle might feel productive, but it could be less effective than expected if the interest continues to climb faster than you can pay it down.

Similarly, economic downturns can impact job security and income stability. If a recession is on the horizon, it might be wiser to temporarily slow down debt payments and focus on building an emergency fund. This isn’t about giving up; it’s about risk management. A sudden job loss with no savings could force you into more debt, erasing years of progress. Market awareness allows you to anticipate these risks and adapt your strategy accordingly. It shifts repayment from a rigid, one-size-fits-all plan to a dynamic process that responds to real-world conditions.

Another example is inflation. When prices rise across the board, your income may not keep pace, making it harder to free up cash for debt repayment. But understanding inflation trends can help you make proactive choices. For instance, if you expect food and fuel costs to remain high, you can adjust your budget early, avoid taking on new debt, and prioritize paying down high-interest balances before they grow further. Market awareness turns you from a passive borrower into an informed decision-maker, someone who sees the bigger picture and acts with intention.

The First Signal: Learning to Read Economic Clues

I didn’t have a degree in economics, but I realized I didn’t need one to understand the basic signals the economy was sending. The first step was learning to recognize early warning signs—simple indicators that anyone can monitor without specialized knowledge. These aren’t complex data points requiring advanced analysis; they’re real-world trends reflected in news, employment reports, and everyday conversations.

One of the most accessible signals is the job market. When layoffs are announced in major industries, or when hiring slows down in your region, it can be a sign of economic stress. I started paying attention to local news and national employment reports. When I noticed that several companies in my area had frozen hiring, I took it as a cue to tighten my budget and pause plans to pay extra toward my car loan. I didn’t know a recession was coming, but I knew the environment was becoming less stable, and I needed to protect my financial position.

Consumer spending is another clue. When people start cutting back on non-essential purchases—delaying vacations, buying fewer clothes, or eating out less—it often reflects broader financial caution. I observed this in my own social circle and in retail trends. When department stores announced lower sales, it signaled that households were under pressure. This reinforced my decision to delay any new purchases and focus on reducing my existing debt burden before taking on more obligations.

Perhaps the most direct signal came from central bank announcements. These institutions set benchmark interest rates that influence everything from credit cards to mortgages. I began following their meeting schedules and reading summaries of their decisions. When the central bank indicated a shift toward higher rates to control inflation, I knew it was time to act. I contacted my credit card issuer to ask about fixed-rate balance transfer options and explored personal loans with fixed terms to lock in lower rates before they increased further. I wasn’t predicting the future with certainty, but I was responding to clear signals that could affect my finances.

Learning to read these clues didn’t require hours of research or expensive subscriptions. It was about developing a habit of awareness—a way of staying informed without becoming overwhelmed. Over time, I began to see patterns. Economic conditions didn’t change overnight, but they did shift gradually, and those shifts created windows of opportunity or moments to exercise caution. By paying attention, I could make smarter decisions about when to accelerate repayment and when to hold back.

Building a Smarter Repayment Strategy

With a better understanding of economic signals, I shifted from a rigid repayment plan to a more flexible, responsive strategy. Instead of blindly following a schedule, I began aligning my debt payments with the broader financial environment. This didn’t mean abandoning discipline; it meant applying it more intelligently. Just as a sailor adjusts the sails based on wind direction, I learned to adjust my financial efforts based on economic conditions.

During periods of economic stability—when my income was steady, interest rates were low, and inflation was under control—I increased my debt payments. I directed extra funds toward high-interest balances, knowing that the environment supported aggressive repayment. These were the times to make meaningful progress, to reduce principal quickly and minimize the total interest paid over time. I treated these phases like financial growing seasons—times to plant seeds of progress that would yield long-term benefits.

Conversely, when warning signs appeared—rising unemployment, rate hikes, or market volatility—I adjusted my approach. I didn’t stop paying my debts, but I prioritized stability over speed. I focused on maintaining minimum payments, protecting my credit score, and building a small emergency buffer. This wasn’t defeat; it was strategic caution. I understood that pushing too hard during uncertain times could backfire if an unexpected expense arose or my income dipped. By slowing down temporarily, I preserved my financial resilience and avoided setbacks that could take months to recover from.

One of the most effective moves I made was refinancing my personal loan when interest rates were still favorable. I researched lenders offering fixed-rate loans with lower APRs and transferred my balance before rates climbed further. This reduced my monthly payment and locked in a predictable repayment schedule, giving me breathing room. Later, when inflation eased and my work hours increased, I resumed higher payments, using the extra income to accelerate repayment without straining my budget.

This adaptive strategy required patience and discipline, but it also brought a sense of control. I was no longer reacting to crises; I was planning ahead. I set personal rules: no major repayment increases during rate hike cycles, no new debt during economic downturns, and always maintaining a small cushion. These guidelines weren’t strict laws, but flexible principles that helped me stay on track without ignoring reality. Over time, this approach reduced both my financial risk and my anxiety.

Balancing Risk and Progress: The Discipline of Timing

One of the hardest lessons I learned was that consistency in debt repayment doesn’t mean pushing forward at the same pace no matter what. True financial discipline includes knowing when to pause, reassess, and adjust. Blind persistence can lead to burnout or, worse, new debt if you overextend yourself during tough times. The key is balancing progress with protection.

There was a period when I considered using my tax refund to make a large lump-sum payment on my credit card. It felt like the responsible thing to do—a chance to make a big dent in the balance. But at the same time, news reports were warning of a possible recession, and my employer had mentioned potential layoffs. I hesitated. Instead of sending the entire refund to my credit card, I split it: half went toward the debt, and half went into a high-yield savings account as an emergency fund. It wasn’t the fastest way to reduce debt, but it was the safest. A few months later, my husband had an unexpected medical bill, and that savings cushion prevented us from charging more to the card.

This experience taught me that timing is a form of financial wisdom. Making extra payments feels rewarding, but it’s not always the best move if it leaves you vulnerable. Market forecasting helped me see that financial health isn’t just about numbers on a statement; it’s about stability, security, and peace of mind. By anticipating potential risks, I could make choices that protected my progress instead of jeopardizing it.

Another example was deciding not to consolidate my debt during a period of rising rates. A friend suggested a balance transfer card with a 0% introductory rate, but I noticed that the standard rate after the promotional period was much higher than my current loan. I also read that rates were expected to continue climbing. I declined the offer, knowing that if I couldn’t pay off the balance during the introductory period, I could end up with even higher interest later. Again, it wasn’t the most aggressive option, but it was the most cautious and informed one.

This balance between action and caution became a core part of my strategy. I tracked my progress, celebrated small wins, but never let momentum override judgment. I learned to ask not just “Can I afford this payment?” but “Is this the right time for this payment?” That subtle shift in thinking made all the difference. It turned debt repayment from a stressful race into a thoughtful journey.

Tools and Habits That Keep You Ahead

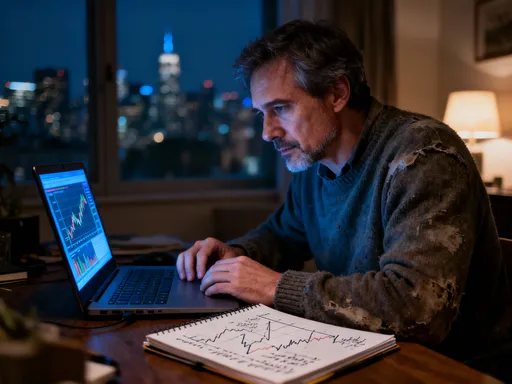

Staying informed about economic trends doesn’t require expensive tools or hours of daily research. What matters is building simple, sustainable habits that keep you aware without causing stress. I started with small changes: setting aside ten minutes each week to read a summary of economic news, following reliable financial websites, and signing up for free email updates from trusted sources.

One of the most helpful tools I discovered was the free economic calendar available on several financial websites. It lists key events like central bank meetings, employment reports, and inflation data releases. I didn’t analyze every number, but I noted when major announcements were scheduled. If a rate decision was coming up, I made sure to review my debt strategy beforehand. This simple habit kept me from being caught off guard by sudden changes.

I also set personal alerts on my phone. For example, when inflation data was released, I received a brief summary from a news app. If major job reports showed weakness, I took it as a reminder to review my emergency fund. These alerts weren’t constant interruptions; they were gentle nudges that kept me connected to the bigger picture. I avoided obsessing over daily market movements, focusing instead on trends that could affect my financial decisions over weeks or months.

Another habit was discussing economic news with my spouse during our weekly money check-ins. We didn’t need to agree on everything, but talking through what we were seeing helped us stay aligned on our financial goals. It also made the process feel less isolating. Financial stress often thrives in silence, but sharing concerns and observations built a sense of teamwork.

Most importantly, I avoided information overload. I didn’t follow every financial influencer or try to predict stock market swings. My focus remained narrow: how economic trends could impact my income, expenses, and debt. This clarity kept me from feeling overwhelmed. Staying informed wasn’t about becoming an expert; it was about being prepared.

From Debt to Financial Clarity: A New Mindset

Looking back, the journey from debt to financial stability wasn’t just about paying off balances. It was about transforming my relationship with money. I went from feeling helpless to feeling empowered, from reacting to crises to planning with confidence. The real victory wasn’t the last payment I made; it was the shift in mindset that made it possible.

Market awareness didn’t give me the ability to predict the future perfectly. No one can do that. But it gave me something more valuable: the ability to make better decisions in the present. I learned to see my finances as part of a larger system, influenced by forces I couldn’t control but could respond to. That awareness reduced my fear and increased my sense of agency.

Today, I’m debt-free, but I still follow economic trends. Not because I’m preparing for disaster, but because it helps me stay grounded and intentional. I apply the same principles to saving, budgeting, and planning for the future. I’ve built a cushion, diversified my income, and made peace with the fact that financial life has seasons—some for growth, some for protection.

My story isn’t unique. Millions of people struggle with debt, and many feel trapped by circumstances beyond their control. But I’ve learned that while we can’t control the economy, we can learn to read its signals and respond with wisdom. Financial resilience isn’t about avoiding challenges; it’s about navigating them with clarity and courage. And that’s a lesson worth carrying forward, long after the last bill is paid.