How I Crushed My Debt While Markets Shifted – A Real Strategy

Paying off debt felt impossible when markets kept swinging and expenses piled up. I tried every trick—budgeting apps, side gigs, even cutting out coffee—and still fell short. Then I changed my approach: instead of ignoring the economy, I used market signals to time my repayments smarter. This isn’t a get-rich-quick scheme. It’s about aligning debt payoff with real financial conditions. Here’s how I did it—and why it finally worked.

The Breaking Point: When Debt and Market Chaos Collided

There was a moment, not long ago, when I sat at my kitchen table staring at a stack of bills, wondering how I had fallen so far behind. My credit card balances had surged after a sudden job cutback, and my variable-rate personal loan had quietly climbed from 6.9% to nearly 12% in just six months as interest rates rose. The minimum payments alone consumed 47% of my take-home pay. I had been diligent—tracking every dollar, skipping dinners out, even selling old furniture—but the ground kept shifting beneath me. Inflation pushed grocery and utility costs higher, and my side gig income dipped when demand slowed. That’s when I realized something fundamental: traditional debt advice wasn’t built for volatile times. Telling someone to “just pay more” when their income is shrinking and borrowing costs are rising isn’t helpful—it’s discouraging. I needed a smarter way, one that didn’t ignore the larger financial environment but instead worked with it.

For years, I believed debt freedom was purely a test of discipline. I thought if I just cut more, earned more, and pushed harder, I’d eventually break free. But the reality of modern personal finance is more complex. Economic forces—interest rate cycles, employment trends, inflation, and market volatility—directly impact our ability to manage debt. When I stopped treating my finances like a closed system and started seeing them as part of a broader economic landscape, everything changed. I began asking questions I’d never considered before: Was now really the best time to throw extra money at my loan? What if a recession hit and I lost my income stream? Could I time my repayments to align with lower borrowing costs or stronger job security? These weren’t excuses to delay—I still wanted to be debt-free—but I wanted to do it in a way that minimized risk and maximized long-term stability. That shift in mindset was the turning point.

Rethinking Debt Repayment: Strategy Over Sheer Willpower

Most financial advice treats debt repayment as a moral issue—a matter of willpower, sacrifice, and persistence. While those qualities matter, they’re not enough when external forces are working against you. I learned this the hard way during a period of high market volatility. I had committed to paying an extra $300 a month toward my highest-interest card, only to face a three-month income dip when my freelance clients paused projects. I kept making the extra payments anyway, draining my checking account and dipping into a small emergency cushion. By the end of that stretch, I was stressed, broke, and no closer to being free of debt. Worse, when an unexpected medical bill arrived, I had no buffer and had to put it on another card—undoing months of progress.

That experience taught me a crucial lesson: aggressive repayment without flexibility can backfire. A rigid, all-in approach ignores the reality that life—and the economy—isn’t linear. Instead of fighting the cycle, I decided to work with it. I developed a dynamic repayment strategy based on three core factors: income stability, interest rate trends, and personal cash flow. When my job felt secure and my hours were consistent, I increased extra payments. When layoffs were being reported in my industry or my side income dipped, I scaled back to minimums and focused on preserving liquidity. This wasn’t giving up—it was adapting. By matching my repayment pace to my actual financial conditions, I reduced stress, avoided new debt, and ultimately paid off more over time because I didn’t have to backtrack.

Another key insight was recognizing that not all debt behaves the same. Fixed-rate loans, like my auto loan, were predictable and easier to plan around. But variable-rate debt, especially credit cards and some personal loans, could change with the Federal Reserve’s rate decisions. I began tracking rate forecasts and refinancing opportunities. When I saw rates peaking, I locked in a fixed-rate consolidation loan at 8.5%, which gave me predictable payments and protection from further hikes. This strategic move saved me hundreds in interest and gave me breathing room to focus on other priorities. Strategy, not just effort, became my real advantage.

Reading the Market: Signals That Guide Smart Payoff Moves

You don’t need a finance degree to understand the basic signals the economy sends. I started paying attention to three key indicators that helped me time my repayment decisions more effectively. The first was employment trends. When major companies in my region began announcing layoffs or hiring freezes, I took it as a warning sign. I didn’t panic, but I did adjust—pausing extra payments and reinforcing my emergency fund. Conversely, when job openings increased and unemployment dipped, I saw it as a green light to accelerate debt payoff, knowing my income was more secure.

The second signal I tracked was bond yields, particularly the 10-year Treasury note. While that might sound technical, it’s actually a reliable proxy for broader interest rate trends. When yields were falling, it often signaled that borrowing costs might soon decline. I used that as a cue to explore refinancing options. For example, when the 10-year yield dropped from 3.8% to 2.9% over a few months, I refinanced my personal loan through a credit union, cutting my rate by nearly two percentage points. That single move saved me over $1,200 in interest over three years. I didn’t need to predict the market—just respond to its direction.

The third indicator was consumer confidence. When surveys showed people feeling pessimistic about the economy, spending dropped, and job markets softened. I viewed those periods as times to conserve cash. When confidence rebounded, I saw opportunity. I used free tools like the Conference Board’s Consumer Confidence Index and the Bureau of Labor Statistics’ employment reports—publicly available and easy to understand. These weren’t crystal balls, but they provided a framework for making more informed decisions. Instead of reacting emotionally to market headlines, I had a system. That shift—from reactive to responsive—was transformative.

Balancing Risk and Reward: Protecting Yourself While Paying Down

One of my biggest financial mistakes was treating debt payoff as the only goal, to the exclusion of all other priorities. I remember a time when I was so focused on eliminating a $7,000 credit card balance that I drained my $3,000 emergency fund to make a final payment. I felt victorious—until two weeks later, when my car’s transmission failed. With no savings, I had no choice but to put the $2,800 repair on another card, immediately undoing my progress. That experience was humbling. I had won a battle but lost sight of the war: long-term financial health.

From that point on, I made risk management a core part of my debt strategy. I rebuilt my emergency fund to cover three to six months of essential expenses, even while still paying off debt. I also adopted a “tiered repayment” approach. During stable periods—when I had steady income, no major expenses expected, and positive economic signals—I directed extra money toward debt. But when uncertainty rose—like during a recession warning or a personal health issue—I scaled back to minimum payments and protected my liquidity. This wasn’t procrastination; it was prudence. I treated financial resilience as equally important as debt reduction.

I also diversified my safety nets. In addition to cash savings, I made sure I had access to low-interest credit options, like a 0% intro APR balance transfer card or a home equity line of credit (HELOC), as a backup—not for spending, but for emergencies. Knowing I had options reduced anxiety and prevented rash decisions. I learned that the most successful debt payoff plans aren’t the fastest—they’re the ones that survive real life. By building in flexibility and protection, I avoided the cycle of progress and setback that had trapped me before.

The Payoff Playbook: Practical Steps That Actually Work

Over time, I developed a four-phase system that brought structure and clarity to my debt journey. The first phase was assess. I listed every debt—balances, interest rates, minimum payments, and due dates. I also mapped my income sources, monthly expenses, and savings. This gave me a clear picture of where I stood. I used a simple spreadsheet, updated monthly, to track progress. Knowledge was power; I couldn’t fix what I didn’t understand.

The second phase was stabilize. This meant securing my income, reducing interest costs, and building a small emergency buffer. I negotiated with creditors to lower rates, transferred high-interest balances to 0% intro APR cards, and refinanced where possible. I also took on a part-time remote role to add stability. Even small steps—like switching to a cheaper phone plan or bundling insurance—freed up cash. The goal wasn’t to eliminate debt yet, but to create a stable foundation.

Phase three was accelerate. This only began when conditions were favorable—steady income, low market volatility, and falling or stable interest rates. I used the debt avalanche method, focusing extra payments on the highest-interest debt first, which saved me the most in interest over time. I set up automatic transfers so payments happened without effort. During this phase, I paid off $18,000 in 14 months—not by earning more, but by timing and discipline.

The final phase was lock in. Once a debt was paid, I didn’t celebrate by spending. Instead, I redirected the payment amount into savings or investments. For example, when my $400-a-month loan was gone, I moved that $400 into a high-yield savings account. This “invisible raise” helped me build wealth without changing my lifestyle. The system worked because it was flexible, data-informed, and designed for real life—not a textbook ideal.

When to Pause—and When to Push

One of the most liberating realizations was that consistent progress doesn’t require constant action. There were months when I intentionally paused extra debt payments—not because I lacked motivation, but because it was the smart financial move. During a period of rising unemployment in my sector, I paused extra payments and focused on job security and cash reserves. I didn’t stop paying—I kept up minimums—but I didn’t stretch myself thin. That restraint protected me when my hours were temporarily reduced. Later, when the job market improved and I received a modest bonus, I doubled my extra payment for three months, making significant headway.

This rhythm—pause when risk is high, push when conditions are strong—created a sustainable pace. I stopped feeling guilty for not paying extra every single month. Instead, I trusted my system. I began to see financial fitness like physical fitness: it’s not about sprinting every day, but about pacing, recovery, and long-term consistency. By aligning my repayment efforts with economic and personal realities, I avoided burnout and maintained momentum. The result? I paid off $31,000 in consumer debt in under three years, without taking on new debt or relying on windfalls.

This approach also improved my relationship with money. I stopped viewing debt as a personal failure and started seeing it as a financial condition to be managed. I became more patient, more strategic, and less reactive. I didn’t need perfection—just progress with protection. That balance made all the difference.

From Debt-Free to Financial Momentum: What Comes After

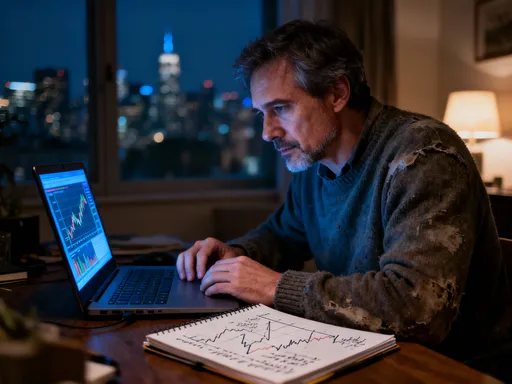

Reaching zero debt wasn’t an ending—it was a transformation. For the first time in years, I had financial breathing room. But I didn’t stop there. I took the same strategic mindset I’d used to pay off debt and applied it to building wealth. I redirected my former debt payments into low-cost index funds, starting with $400 a month into a broad-market ETF. I didn’t try to time the market for gains, but I did use market conditions to guide my contributions. During periods of high volatility and lower prices, I increased contributions slightly, taking advantage of dollar-cost averaging in a thoughtful way.

I also continued to monitor economic signals. When interest rates were low, I explored fixed-income options like CDs and Treasury securities to lock in gains. When inflation rose, I adjusted my portfolio to include assets that historically perform well in those conditions, like TIPS (Treasury Inflation-Protected Securities) and dividend-paying stocks. The same awareness that helped me avoid overextending during uncertain times now helped me invest with confidence.

Most importantly, I maintained my emergency fund and avoided lifestyle inflation. I didn’t buy a new car or take an expensive vacation. Instead, I let my financial discipline compound. Within two years, I had saved enough for a home down payment and started a small education fund for my children. The habits I built during my debt journey—awareness, patience, flexibility—became the foundation of lasting financial health.

Looking back, I realize that crushing my debt wasn’t about extreme sacrifice or sudden luck. It was about changing my relationship with money—seeing it not as something to fear or control through willpower alone, but as a system to understand and navigate wisely. By aligning my actions with real financial conditions, I didn’t just survive market shifts—I used them to my advantage. That’s the strategy that worked. And it’s one anyone can adopt, not with perfection, but with intention.