How I Finally Tamed My Debt Using These Simple Financial Tools

Remember that sinking feeling when bills pile up and your wallet feels empty? I’ve been there. As a beginner drowning in debt, I didn’t know where to start—until I discovered practical financial tools that actually work. No magic tricks, just smart, proven strategies. This is my journey from stress to control, and how you can use the same tools to regain your financial freedom. It wasn’t an overnight change, but a series of small, consistent decisions backed by the right support systems. If you're tired of living paycheck to paycheck and ready to take back control, this is your roadmap. The path out of debt isn’t about earning more—it’s about managing what you have with clarity, discipline, and the right tools.

The Wake-Up Call: Facing Debt Head-On

It happened on a Tuesday evening, like so many ordinary moments that carry extraordinary weight. I sat at the kitchen table, a stack of unopened envelopes in front of me—credit card statements, a medical bill reminder, a notice from a loan servicer. My hands trembled slightly as I opened the first one. The number was higher than I remembered. The second was worse. By the third, I felt a familiar knot tighten in my stomach. I wasn’t just behind; I was in deep, and I had been ignoring it for months. That night, I didn’t sleep. Instead, I stared at the ceiling, replaying every purchase I couldn’t justify, every promise I’d made to myself about “getting it together next month.”

What I realized in those quiet hours wasn’t just that I had debt—but that I had been avoiding it. Like many people, I believed that if I didn’t look at the numbers, they wouldn’t grow. Of course, that wasn’t true. Debt doesn’t disappear when ignored; it compounds. Interest accrues, late fees pile up, and the emotional burden grows heavier with every passing day. The real turning point wasn’t a sudden windfall or a financial epiphany—it was the decision to stop running. I made a choice: I would face my debt, not with shame, but with honesty. And that shift in mindset was the first, most crucial step toward freedom.

For years, I thought financial control was only for people with high incomes or special knowledge. I believed budgeting was for accountants, not mothers juggling grocery lists and carpool schedules. But the truth is, financial stress doesn’t discriminate. It affects people from all walks of life, especially those managing households on tight margins. What separates those who escape debt from those who remain trapped isn’t luck—it’s action. And action begins with awareness. By naming the problem, I took power back. I wasn’t broken; I was learning. And that simple reframe—seeing debt not as a moral failure but as a solvable challenge—changed everything.

Mapping the Terrain: Understanding Your Debt

Before you can fix a problem, you need to understand it. That’s why the second step in my journey wasn’t paying anything off—it was gathering all the facts. I cleared the dining table and spread out every piece of paper related to money: credit card bills, student loan statements, a personal loan from a credit union, even an old medical bill I’d forgotten about. I listed each debt separately, writing down the creditor, the current balance, the interest rate, and the minimum monthly payment. At first, the process felt overwhelming. Seeing it all in one place was painful. But within an hour, something shifted. The fog of confusion began to lift.

Clarity replaced panic. Instead of a vague sense of dread, I had data. And data is power. I discovered that I owed $23,450 across six different accounts. The highest interest rate was 26.99% on a store credit card I’d opened during a holiday sale five years earlier. The smallest balance was just $387, but it carried an 18% rate. I hadn’t realized how much I was paying in interest each month—nearly $400, just to stay in place. That was more than my car payment. This exercise didn’t solve my debt, but it gave me a map. And with a map, even the longest journey becomes manageable.

Many people avoid this step because it feels like facing a mirror they’re not ready to see. But here’s the truth: you can’t manage what you don’t measure. By documenting every debt, you remove emotion from the equation and create a foundation for strategy. It also helps you identify patterns. For me, I saw that most of my high-interest debt came from convenience purchases—online shopping, takeout meals, small luxuries that added up over time. Understanding the source of the debt made it easier to commit to change. This wasn’t just about paying bills; it was about changing behavior. And the first tool I used wasn’t an app or a calculator—it was a notebook and a pen.

Budgeting Without the Boredom: Making It Real

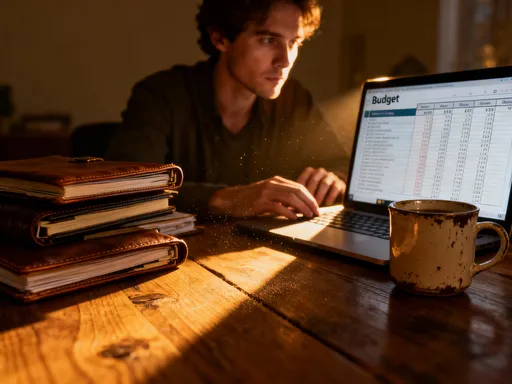

Budgeting used to sound like a punishment to me. I imagined rigid rules, forbidden purchases, and a life stripped of joy. But the truth is, a good budget isn’t about restriction—it’s about intention. It’s about deciding where your money goes, instead of wondering where it went. My breakthrough came when I stopped thinking of a budget as a diet and started seeing it as a plan. And like any good plan, it needed to reflect reality, not perfection.

I tried several methods before finding one that worked. At first, I used a spreadsheet, carefully listing every income source and expense. It was accurate, but it took too long to update. Life moved faster than my ability to log every coffee or gas fill-up. Then I tried a popular budgeting app that categorized spending automatically. That helped, but it felt impersonal. I needed something that balanced simplicity with insight. What finally clicked was a hybrid approach: I used a mobile app to track daily spending in real time, but I reviewed it weekly with a simple handwritten summary. This kept me engaged without overwhelming me.

The key was customization. I allocated funds for groceries, utilities, transportation, and even a small “fun money” category. That last one was essential. When I denied myself everything, I eventually rebelled and overspent. But when I gave myself permission to spend $50 a month on whatever I wanted—books, a manicure, a nice dinner—I stayed within limits. The budget became sustainable because it respected my life as it actually was. Over time, I found ways to reduce expenses—switching to a cheaper phone plan, buying groceries in bulk, canceling unused subscriptions. These small savings, often less than $20 a month, added up. Within six months, I freed up an extra $180 each month to put toward debt. That wasn’t magic—it was math, made possible by awareness.

The Debt Snowball vs. Avalanche: Which One Fits You?

With a clear picture of my debt and a working budget, I faced a critical question: where to start? I’d heard of two main strategies—the debt snowball and the debt avalanche. Both are effective, but they work in different ways and appeal to different personalities. The debt snowball method involves paying off the smallest balances first, regardless of interest rate, while making minimum payments on everything else. The idea is to build momentum through quick wins. The debt avalanche, on the other hand, targets the highest interest rates first, which saves more money over time but may take longer to see results.

I researched both and realized this wasn’t just a financial decision—it was a psychological one. Mathematically, the avalanche is more efficient. By eliminating high-interest debt first, you reduce the total amount of interest paid. In my case, that would mean attacking the store credit card with the 26.99% rate right away. But I also knew myself. I needed motivation. I needed to see progress quickly, or I’d lose steam. That’s why I chose the snowball method. I started with the $387 medical bill. It wasn’t the most expensive, but paying it off gave me a rush of accomplishment. That small victory made the next step feel possible.

After that, I tackled a $650 credit card balance. Then a $920 personal loan. Each time I paid off an account, I rolled the payment amount into the next debt. That’s the power of the snowball—it grows as you go. Even though I was still paying interest on larger balances, the emotional boost kept me going. Studies from financial experts show that behavioral momentum is a key factor in long-term debt repayment success. People who use the snowball method are more likely to stick with it, not because it’s the most efficient, but because it feels rewarding. For me, that made all the difference. You don’t have to choose based on what’s theoretically best—choose what works for your mindset.

Automated Tools That Do the Work for You

One of the biggest obstacles to staying on track was consistency. Life gets busy. Some months, I forgot to make extra payments. Other months, unexpected expenses drained my extra cash. That’s when I turned to automation. Technology became my silent partner in the debt repayment journey. I set up automatic payments through my bank, ensuring that at least the minimum amount was paid on time every month. Late fees disappeared. My credit score began to improve.

But I went further. I used a financial app that allowed me to schedule recurring extra payments toward my snowball target. Every payday, $100 was automatically sent to the next smallest debt. I didn’t have to think about it. I didn’t have to log in. The money moved before I had a chance to spend it. This removed temptation and decision fatigue. I also enabled a “round-up” feature on my checking account, where every purchase was rounded up to the nearest dollar, and the difference was saved. Over a month, that added up to about $45—money I never missed, but that steadily built a buffer.

Some people worry that automation removes control, but for me, it gave me more control. By programming my finances, I ensured that my priorities were honored, even on chaotic days. I also used a debt tracker app that visualized my progress with a simple bar chart. Watching the bars shrink each month was incredibly motivating. These tools didn’t replace discipline—they supported it. They turned a daunting, emotional process into a systematic, almost effortless routine. And that’s the secret: the best financial tools don’t require constant willpower. They work quietly in the background, helping you succeed without burning out.

Emergency Funds: The Hidden Debt Fighter

Just when I thought I was making progress, my car’s transmission failed. The repair cost $1,200—more than I had in savings. I felt the old panic rising. Would I have to put it on a credit card? Would all my progress be undone? That moment taught me a crucial lesson: no debt repayment plan is complete without an emergency fund. Without one, any surprise—a medical bill, a home repair, a job loss—can send you back into debt.

I used the insurance payout to cover part of the repair and adjusted my budget to pay the rest over three months. But I also made a new rule: I would start building a small emergency fund, even while paying off debt. Financial experts often recommend saving three to six months of expenses, but that felt impossible at the time. So I started small. My first goal was $500—enough to cover minor emergencies like car trouble or a dentist visit. I set up a separate savings account and automated a $25 transfer each week. It took less than five months to reach my goal.

Having that $500 didn’t make me rich, but it made me resilient. When my washing machine broke six months later, I paid for the repair without hesitation. No stress. No new debt. That small fund became a psychological safety net. It reduced anxiety and gave me confidence. Over time, I increased the target to $1,000, then $2,000. The key was consistency, not size. Even as I paid off debt, I protected my progress by building protection against the unexpected. This dual focus—attacking debt while creating a cushion—was what made my financial turnaround sustainable. You don’t have to choose between paying down debt and saving; you can do both, slowly and steadily.

Staying on Track: Habits That Keep You Free

After 18 months, I made my final debt payment. It wasn’t a large amount—just $217 on a student loan—but it represented freedom. I remember calling the servicer, confirming the balance was zero, and then sitting in silence for a full minute. The relief was profound. But I also knew the journey wasn’t over. Financial health isn’t a destination; it’s a practice. The real test would be maintaining the habits that got me there.

I committed to three simple routines. First, a monthly money check-in. Every first Sunday of the month, I review my budget, track spending, and adjust as needed. It takes less than an hour, but it keeps me aware. Second, I continue to track my net worth quarterly. Watching it grow reinforces good behavior. Third, I practice mindful spending—asking myself before every non-essential purchase: Do I need this? Can I afford it without guilt? Does it align with my values? These habits prevent backsliding.

I also celebrate wisely. When I reached milestones—paying off the first account, building the emergency fund, becoming debt-free—I rewarded myself. But I chose rewards that didn’t undo my progress: a weekend getaway, a new pair of comfortable shoes, a nice dinner out. The key was intentionality. I didn’t let celebration become excess. And I shared my journey with trusted friends, which created accountability. Talking openly about money reduced shame and inspired others to start their own journey. These habits aren’t flashy, but they’re powerful. They turn temporary success into lasting freedom.

From Repayment to Financial Confidence

Looking back, I realize that getting out of debt wasn’t just about money—it was about reclaiming peace of mind. The tools I used—budgeting, the snowball method, automation, emergency savings—were important, but the real change happened within. I learned that financial control isn’t about perfection. It’s about persistence. It’s about showing up, even when you’re tired, even when progress feels slow. It’s about making small, smart choices every day, knowing they add up.

Today, I still use the same tools. My budget is more flexible now, my savings growing. I invest in low-cost index funds, plan for retirement, and enjoy life without guilt. But I never forget where I started. If you’re reading this and feeling overwhelmed, know this: you’re not alone, and you’re not behind. The best time to start was yesterday. The second-best time is today. You don’t need a raise or a miracle. You need a plan, a few simple tools, and the courage to begin. Financial freedom isn’t reserved for the wealthy. It’s available to anyone willing to take the first step—and the next, and the next. One smart choice at a time, you can build a life of confidence, control, and calm. And that’s a future worth working for.